Home to over 150 fintech companies, Kenya has one of the biggest and most developed fintech ecosystems in the African continent, owning to the proliferation of mobile phones and the rise of mobile money.

Similarly to other developing markets, Kenya’s fintech wave has been built on mobile phones, whose adoption in the continent accelerated around the turn of the millennium and are now pervasive.

Telecommunication giant Safaricom recognized early on the potential of mobile phones and the mobile channel to deliver banking and financial services to the masses. In 2007, it launched M-Pesa, a SIM-based mobile banking service that requires no Internet connection and which runs on technology similar to text messaging.

M-Pesa allows users to deposit, withdraw, transfer money, pay for goods and services, access credit and savings, all with a mobile device. It combines Safaricom’s mobile infrastructure with an agent model: Safaricom stores the balance and customers can go to any of 110,000 agents throughout the country to conduct transactions in person.

Since its launch, M-Pesa has spread quickly and expanded to seven countries. By 2010, it had become the most successful mobile-phone-based financial service in the developing world, and as of June 2020, it had more than 30 million active users in Kenya out of a total population of 52 million, according to data from the Communications Authority of Kenya.

Mobile money helps improve financial inclusion

The success of M-Pesa has led many other telcos and banking institutions to follow suit and get into the mobile money business. Equity Bank launched its mobile money service Equitel back in 2015. The company has embraced a locally-focused strategy that has enabled it to capture 22% of the mobile money market in just five years. Today, the company provides a full suite of banking services on mobile devices.

Airtel Kenya and Telkom Kenya are other telcos that operate mobile money services in Kenya.

The rise of mobile money in Kenya has been rightfully credited for numerous advancements in key metrics used to measure economic development.

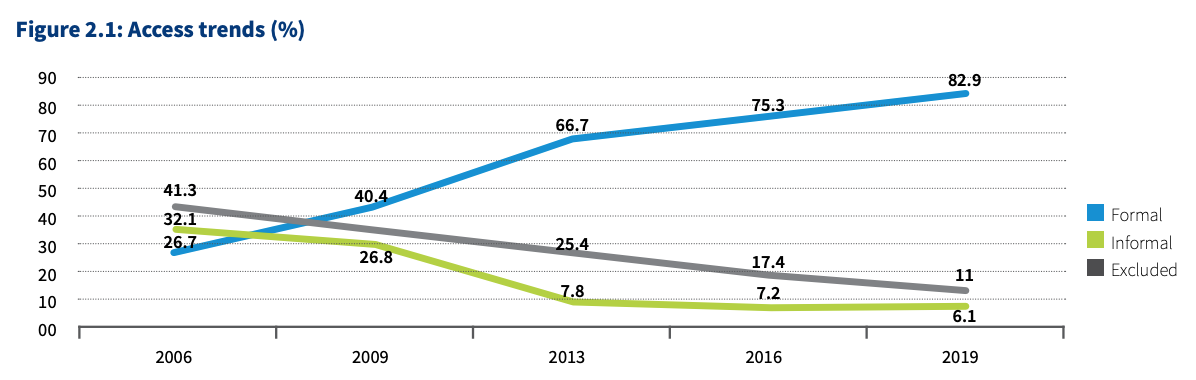

In 2006, formal financial inclusion stood at just 26% in Kenya. Today, the country has the highest rates in sub-Saharan Africa with 82.9% of the adult population having access to at least one financial product, the central bank estimates, and mobile money penetration standing above 100% due to many customers holding multiple SIM cards.

Access to financial services and products, 2006 -2019, Source: 2019 FinAccess Household Survey, The Central Bank of Kenya, Kenya National Bureau of Statistics, FSD Kenya

Kenya’s fintech startups

Mobile money was the spark that ignited the fintech fire in Kenya. Startups like Kopo Kopo have built solution on top of popular mobile money platforms. Founded in 2011, Kopo Kopo started as a digital platform to enable small merchants in Kenya to accept digital payments, primarily for M-Pesa, before expanding to other products including unsecured cash advances, loyalty programs, and more.

Others are going after emerging global trends, including cryptocurrency, insurtech and digital banking. Umba, a company founded in 2011, provides a full service digital banking app. The company, which currently operates in Kenya and Nigeria, raised a US$2 million seed round in December 2020 to expand product capabilities.

In insurtech, Turaco provides an online microinsurance platform for individuals. Founded in 2018, the company specializes in affordable health and life insurance products for lower-income demographics.

Turaco distributes its products through partnerships with local businesses and mobile lending organizations in Kenya and Uganda, and has so far insured over 70,000 people. Turaco closed a US$2 million seed funding round in November 2020 to scale operations in sub-Saharan Africa.

In alternative financing, Pezesha provides a digital platform where micro, small and medium-sized enterprises (MSMEs) are matched with investors, including banks, microfinance institutions and retail lenders, to secure funding. Pezesha was launched in 2017 and since then has funded more than 75,000 loans to MSMEs and disbursed over US$2 million across Kenya. The company has partnered with the likes of Google, PesaPoint, Mastercard and Letshego to expand its reach

Paytech company Cellulant is one of the most established fintech firms in Kenya. Founded in 2004, Cellulant offers a mobile payment and digital commerce ecosystem for businesses. It provides business-to-business (B2B) digital payment services that prompt, collect, settle, and reconcile payments in real-time. Cellulant was named among the Top 50 emerging Fintech companies in the world in KPMG’s 2018 Fintech100 report, and data from Crunchbase suggest that it has raised more US$54 million in funding so far.

Other fintech companies from Kenya include BitPesa, a blockchain payments startup and digital foreign exchange platform, Apollo Agriculture, an online marketplace for farm loans, and INuka Pap, a mobile platform for unsecured personal loans.

According to research conducted by global investment firm Partech Partners, fintech companies in Kenya raised US$198 million in funding 2019. Though data compiled by Disrupt Africa suggests that Kenyan fintechs only raised a little over US$7 million in 2020, funding has significantly picked up this year with startups including Popote, Powered by People and ImaliPay all closing funding rounds in the past two months.

Featured image credit: Photo by Alexander Suhorucov from Pexels

{kind=link}

11 Comments so far

Jump into a conversation