In Israel, the fintech industry is playing an increasingly important role in the country’s economy. In 2021, the sector employed 20,000 people in Israel and contributed about ILS 8.2 billion (US$2.2 billion) to the country’s gross domestic product (GDP), figures that showcase the rising significance of fintech on economic growth, a new report by the Israel Securities Authority, says.

The Israel’s Fintech Industry: A Customer and Market Perspective Analysis report, released last month, reveals that the impact of fintech development has been greater in Israel than in other jurisdictions.

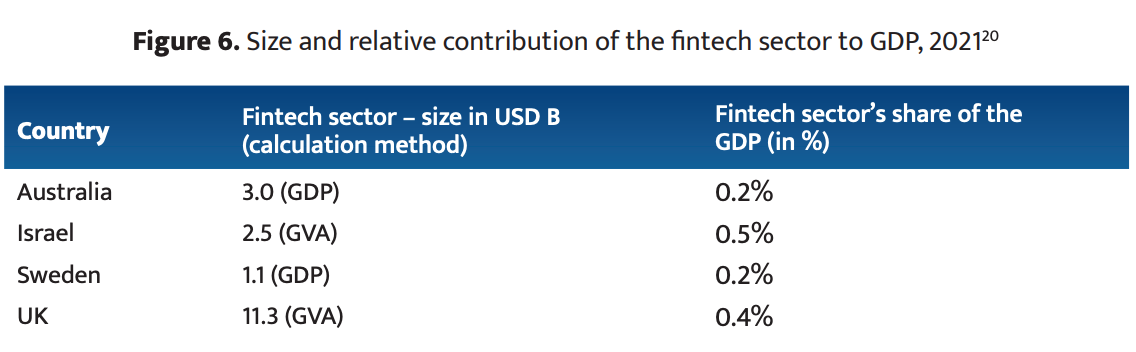

In 2021, fintech contributed to 0.5% of Israel’s total GDP, a proportion that’s higher than international counterparts, including the UK (0.4%), Australia (0.2%) and Sweden (0.2%).

Size and relative contribution of the fintech sector to GDP, 2021, Source: Israel Securities Authority, Jan 2023

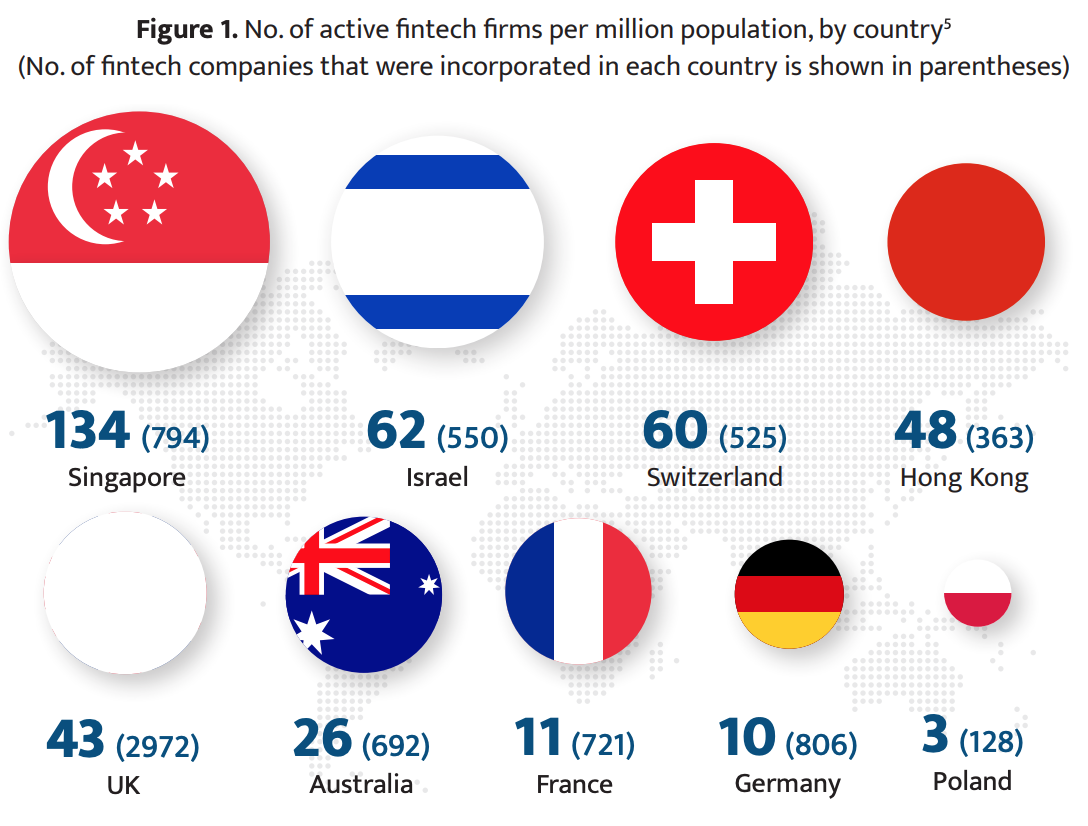

The size of the industry is also substantial too, the analysis found, with some 550 active fintech companies identified by the Israel Securities Authority as of July 2022. The figure makes Israel a notable player in the global fintech scene, being home to a larger number of fintech companies than Hong Kong.

That number is particularly impressive when taking into account Israel’s relatively small population of about 9 million. This number implies a ratio of 62 active fintech companies per million inhabitants, and makes Israel one of the densest fintech markets in the world, surpassing Switzerland (60), the UK (43) and Australia (26), but behind Singapore (134).

Fintech is also contributing considerably to the local job market, employing approximately 20,000 employees in Israel, or 0.5% of all employed individuals in the country.

Number of active fintech firms per million population by country, Source: Israel Securities Authority, Jan 2023

The report, which also looks at the fintech sector’s contribution to consumers, notes that while financial inclusion in Israel stands high and can be compared to rates seen in other developed markets, some deficit can be observed in specific segments of the population, including the Arab community, the ultra-orthodox community and the socioeconomically disadvantaged population.

Against this backdrop, fintech development should be supported to help improve financial inclusion and the financial health of all population groups, the report says.

Fintech also introduces new alternatives to the market. These options are oftentimes more convenient, more efficient and cheaper than traditional financial services. This ultimately leads to increased competition in the finance and banking industry, thus encouraging innovation.

In this context, and considering the potential value that fintech companies could contribute to Israel’s financial market, the report stresses that more work needs to be done to lower the barriers to entry.

Among other things, the financial regulator advises for the completion of a licensing regime for non-bank payment service providers and the establishment of an entity under the Ministry of Finance that would be responsible for overseeing the sector and ensuring that market players are adopting new reforms.

To attract foreign fintech players, the regulator recommends the granting of concessions and exemptions to fintech firms that operate overseas as well as the establishment of a regulatory sandbox to encourage market entry.

Finally, fintech companies should be allowed to offer buy now, pay later (BNPL) arrangements as part of their operations, and should be able to be direct participants in the country’s payment systems, the Israel Securities Authority says.

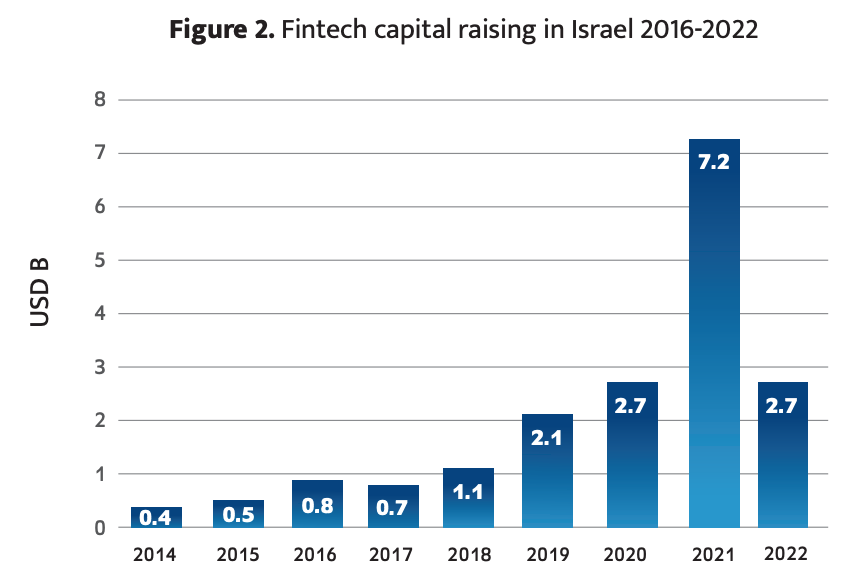

The Israeli fintech sector has risen considerably over the past years. In 2021, companies in the space secured a total of US$7.2 billion, a sum that’s more than threefold the amount raised in the preceding year and more than the total investments in the sector in the five preceding years.

Reflective of global trends, fintech funding dipped last year, decreasing by 62% from 2021 to US$2.7 billion.

Fintech capital raising in Israel 2016-2022, Source: Israel Securities Authority, Jan 2023

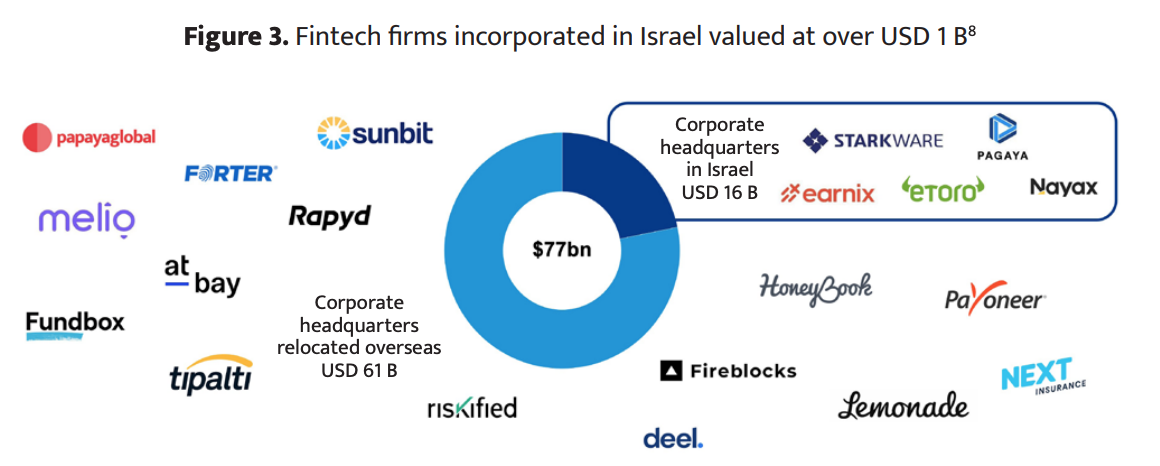

According to the report, a total of 20 fintech unicorns originated from Israel, combining a total valuation of US$77 billion. 15 out of these 20 companies, however, have relocated their headquarters overseas during their growth process. These companies include paytech firm Rapyd, cross-border payment company Payoneer, accounting software provider Tipalti, fraud management specialist Riskified, as well as insurtech firms Lemonade and Next Insurance.

The five fintech unicorns that maintained their corporate headquarters in Israel are social trading and multi-asset investment company eToro, cryptography specialist Starkware, artificial intelligence (AI) lending platform Pagaya, enterprise solutions provider Earnix, and cashless payment solutions provider Nayax.

Fintech firms incorporated in Israel valued at over US$1 billion, Source: Israel Securities Authority, Jan 2023

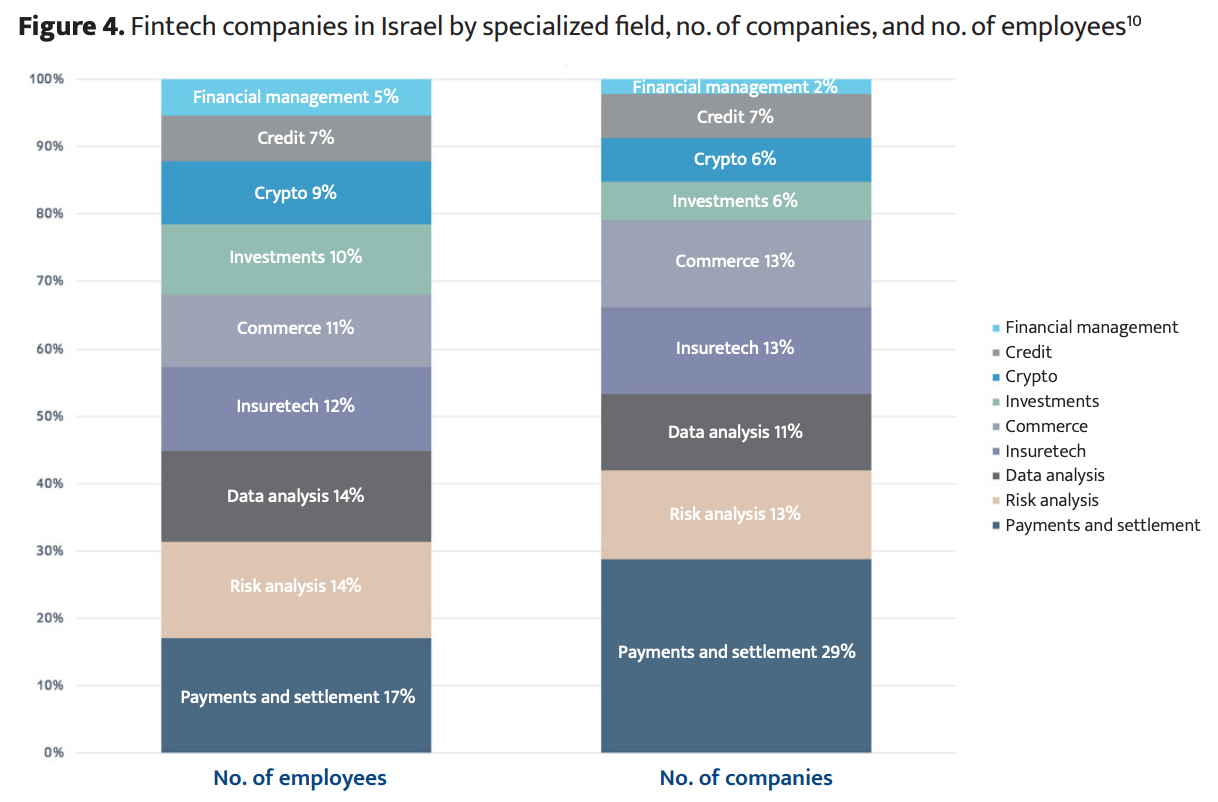

Looking at Israeli fintech startups’ distribution, the report shows that payments and settlement is the largest fintech segment in the country, accounting for 29% of all fintech companies and 17% of the total fintech workforce. The segment is followed by risk analysis, accounting for 13% of all companies and 14% of the workforce. Other prominent segments include data analysis, insurtech and commerce.

Fintech companies in Israel by specialized field, number of companies, and number of employees, Source: Israel Securities Authority, Jan 2023

{kind=link}

No Comments so far

Jump into a conversationNo Comments Yet!

You can be the one to start a conversation.