The digital financial advisory industry is destined for strong growth in the United Arab Emirates (UAE), and while business-to-consumer (B2C) solutions are rapidly gaining traction from the public, business-to-business (B2B) robo-advisor providers are emerging as key enablers for banks and financial institutions, enabling them to quickly deploy powerful platforms.

The UAE market poised for growth

According to Hasan Heider, a partner at venture capital firm 500 Startups, much of the existing banking and wealth management efforts in the Middle East are focused on ultra-high net worth and high net worth individuals, giving digital financial advisory platforms a “massive opportunity” to fill the gap.

“A lot of investors don’t qualify for these wealth management services, and it hasn’t been cost effective for banks to really provide those services to the ‘mass affluent’ market,” Heiser told The National.

Heider has invested in local robo-advisory startup Sarwa, one of the first robo-advisors to launch in the UAE. Sarwa provides a hybrid robo-advisor that uses both a technology and human element to offer affordable and accessible investing, and has around 2,700 registered users. The company is now looking to tap into the underserved population with a mission to “democratize the whole wealth management industry,” according to Nadine Mezher, chief marketing officer and co-founder at Sarwa.

Another robo-advisor has gained considerable traction in the UAE is Wahed Invest, a company founded in the US that offers a Sharia-compliant digital financial advisory platform aimed toward Muslim investors. Wahed Invest hit a US$100 million valuation in November 2018 when it raised US$8 million.

Echoing Heiser, George Triplow, MENA wealth and asset management leader at EY, said that robo-advisors can serve the portion of the population with lower earnings and fewer assets but yet would still be interested in placing their savings.

“Historically, there were two main groups of clients in the Gulf Cooperation Council (GCC) who have investable assets: GCC nationals and high-income expatriates,” Triplow said. “However, a third group is emerging that is attractive to wealth managers and private banks: the affluent segment of upwardly mobile millennials who want to transact business in a different way and communicate with advisors in a different way.”

Why banks must get moving

As robo-advisors make inroads into the UAE, banks and traditional financial institutions too should be looking to get into the game.

In the region, several have begun partnering with tech companies to provide robo-advisory services. These include for instance NBK Capital’s digital investment service NBK Capital SmartWealth in Kuwait which the firm developed in collaboration with Neo Technologies.

But in the UAE, financial institutions have been somewhat slow to wake up to the trend. Yet, with a young, tech-savvy population, growing wealth, and a rising middle class, robo-advisors in the UAE are poised for prime time.

In addition to convenience, affordability and being accessible 24/7, robo-advisors can provide an alternative to the boring long-term savings plans and a much easier entry into the world of passive stock investing considering that most these automated financial planning services offer to invest in exchange traded funds (ETFs) and index funds.

To help banks and financial institutions deal with the daunting and expensive task of building and deploying a robo-advisory platform, several  fintech startups have emerged in recent years to provide them with robust solutions that are easy to integrate.

fintech startups have emerged in recent years to provide them with robust solutions that are easy to integrate.

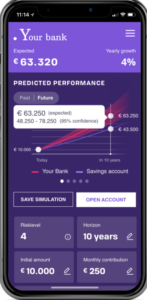

Belgian experts Investsuite for instance offers software solutions that allow financial institutions to quickly begin offering robo-advisor and other digital investment products. The company provides a suite of white-label wealthtech products-as-a-service that includes a robo-advisor, a trading platform, and a “portfolio storyteller” that simplifies portfolio reporting and cuts through the financial jargon.

Investsuite’s “robo-as-a-service” solution allows banks to launch their own robo-advisory product in a cost-effective and timely manner. The solution is flexible and can be implemented and configured in a number of ways including as a fully stand-alone product with dedicated mobile app, or it can be integrated in an existing online brokerage service, or within a bank’s very own mobile platform.

{kind=link}