The Arab Monetary Fund (AMF) has recently issued guidelines regarding distributed ledger technology (DLT) and blockchain in the Middle East for financial services.

Under the “Strategies for Adopting DLT/Blockchain Technologies in Arab Countries” guide, the Arab Regional Fintech Working Group has issued directives on the financial applications of blockchain. It is aimed at bolstering financial and banking services, digital financial transformation and financial inclusion.

With an elaborate overview of DLT and blockchain initiatives in different countries, the guide covers implementation of such applications in the financial sector, alongside action plans and an evaluation matrix as well.

It also discusses integrating DLT and blockchain in the Middle East with other technologies such as AI, big data and IoT, as well as smart contracts, digital signature, key custody and security solutions.

How has DLT and blockchain in the Middle East affected the financial value chain?

Source: AMF

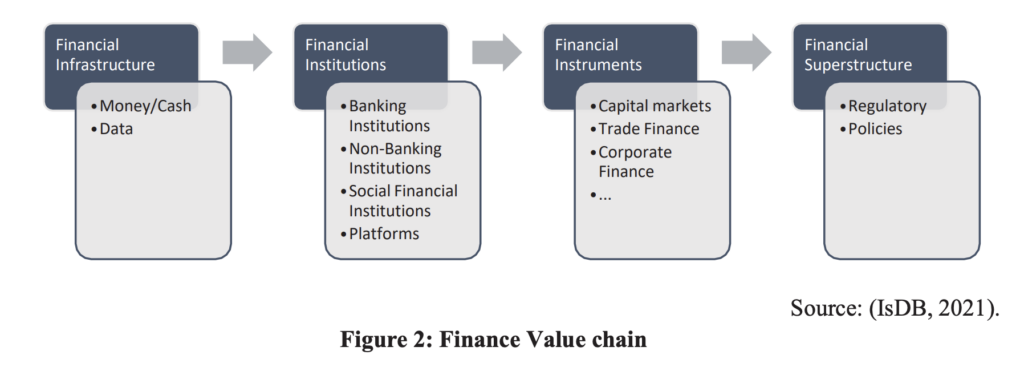

The applications of DLT and blockchain in the financial industry spans for key verticals. With financial infrastructure, DLT and blockchain have turned data into a valuable asset (such as compliance or transaction data) across the value chain, thereby attracting more entrants to solve for this space.

It has also led to a viable alternative to fiat currencies, transforming currency-centric operations such as payments. In addition to automating payments, DLT and blockchain have also helped to increase transparency and trust, the report said.

On the institutional front, DLT and blockchain have also “enabled alternative models for non-bank payment service providers, micro-finance, micro lending and other types of alternative providers for financial services,” the report said.

This has led to an impact across the customer journey, asset management, settlement process, and product offerings. At the same time, however, it has highlighted a growing need for cybersecurity measures and regtech offerings to mitigate fraud and error.

Thirdly, DLT and blockchain have led new financial instruments to come to the fore, such as smart contracts, tokenised loans and funds, reporting tools, and origination, securitisation and servicing platforms.

Finally, when it comes to financial superstructures, DLT and blockchain can help to automate compliance activities such as KYC and onboarding, reporting, and enforcement.

Source: AMF

In this respect, the report points towards the application of DLT for ID verification through unique identifiers for onboarding or account opening

“[The unique identifier] can be stored on a distributed ledger and referenced by any bank in the network. The owner of this unique identifier can use it to submit new account applications and prove his identity universally. The DLT structure removes overlapping KYC and AML compliance checks, reduces the information burden, and accepts banks to disseminate data as it is updated,” the report explains.

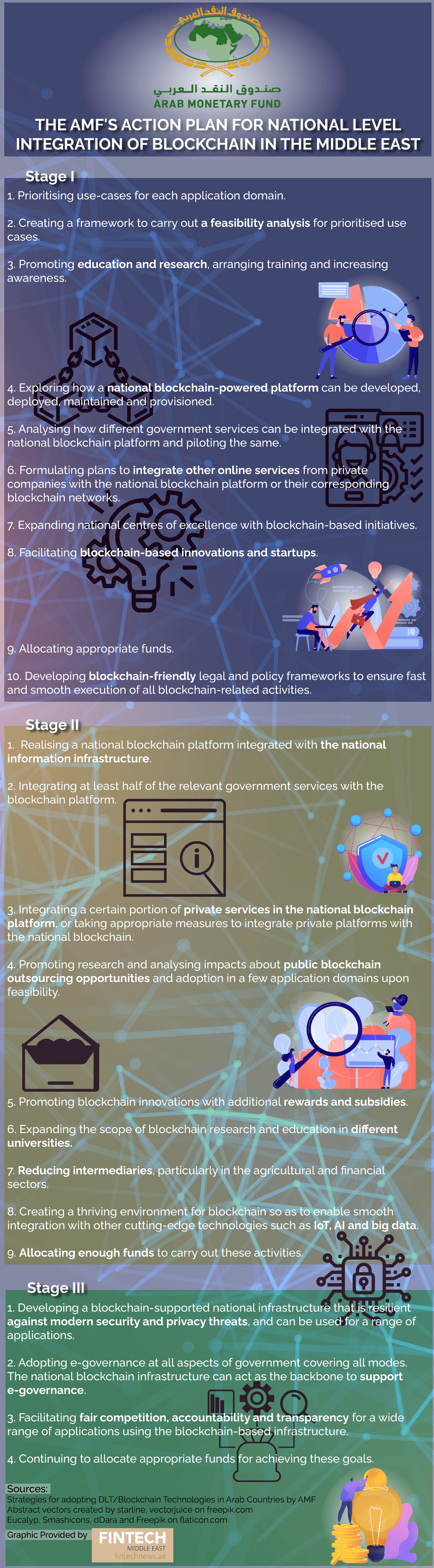

Roadmap For DLT and Blockchain adoption

The AMF recommended a comprehensive action plan to boost DLT and Blockchain adoption in the Middle East. It also suggested that cost and use-case considerations, and embedded supervision, will need to be accounted for.

{kind=link}

No Comments so far

Jump into a conversationNo Comments Yet!

You can be the one to start a conversation.