Over the past few years, Egypt’s fintech sector has grown at a rapid pace as the startup ecosystem thrives and investment surges. In its first industry report, Fintech Egypt, an initiative of the Central Bank of Egypt, delves into that growth, sharing key growth metrics and emerging trends.

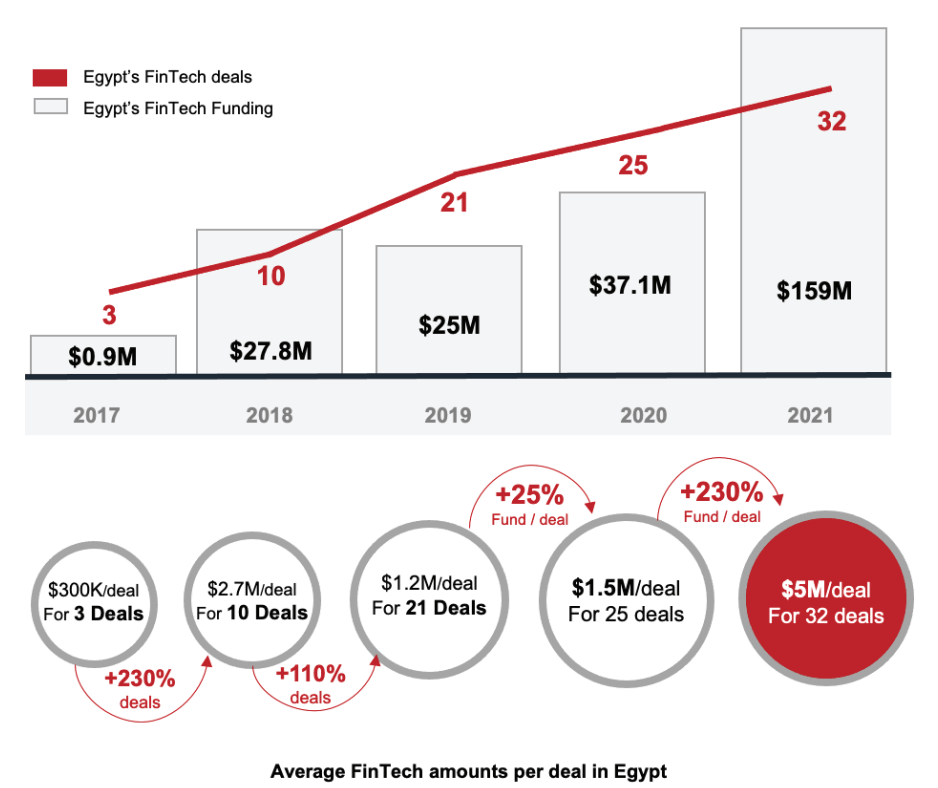

According to the inaugural Egypt Fintech: Landscape Report 2021, Egyptian fintech companies are increasingly catching the eye of the investors community, which poured a new record of US$159 million in 2021, up X4 from just US$37.1 million in 2020.

The figure makes Egypt the fourth largest country in fintech investments in Africa and the second largest country in the Middle East and North Africa (MENA) region, the report says, citing data from MENA-focused startup data platform Magnitt.

Egypt fintech funding between 2017 and 2021, Source: Egypt Fintech: Landscape Report 2021, Fintech Egypt

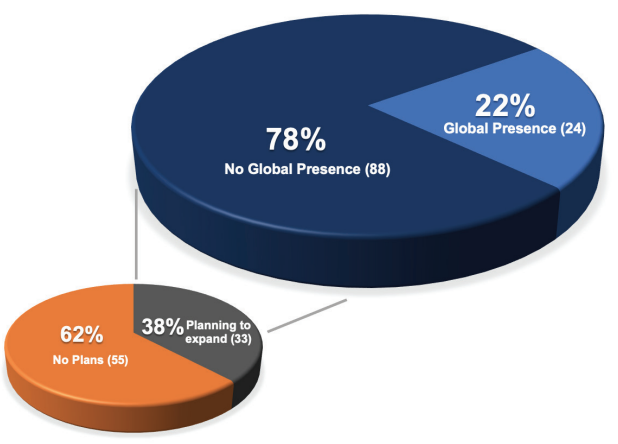

Average ticket size increased more than X3 between 2020 and 2021, indicating that Egyptian fintech companies are maturing and scaling. In fact, 24 startups of 112 fintech startups interviewed as part of the study indicated having expanded regionally and internationally, and now have presence across the Middle East and North Africa (MENA) report, as well as the Gulf Cooperation Council (GCC) and Europe.

Out of the remaining 88, 33 startups said they intend to expand in the upcoming year with a major focus on Africa and MENA, showcasing that Egyptian fintech entrepreneurs have global ambitions.

Egyptian fintech startups with a global presence or planning to expand globally, Source: Egypt Fintech: Landscape Report 2021, Fintech Egypt

Egypt’s fintech startup ecosystem

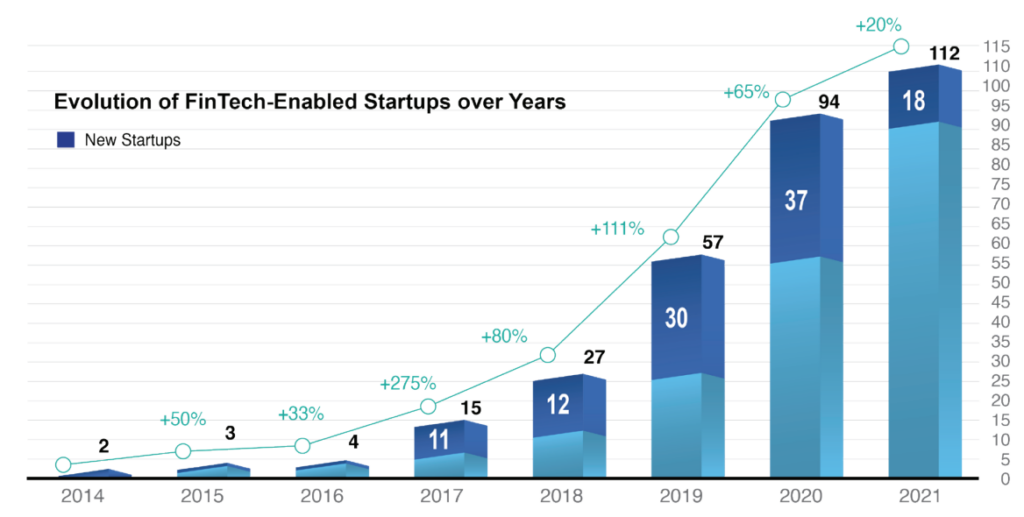

Aside from fintech funding, the report also looks at the domestic startup ecosystem, highlighting the surge in new business creation over the past few years. In 2014, Egypt was home to only two fintech startups, a number that soared to 57 in 2019 and 112 companies by the end of 2021. The figure makes Egypt the fourth largest fintech ecosystem in Africa, the report says.

Evolution of fintech-enabled startups in Egypt since 2014, Source: Egypt Fintech: Landscape Report 2021, Fintech Egypt

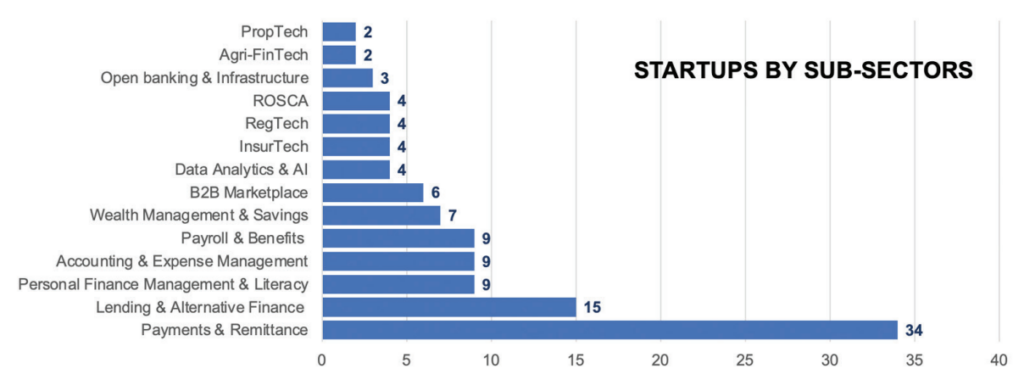

A breakdown by sub-sectors reveals that payments and remittances are currently the most represented fintech segment in Egypt with 34 companies, followed by lending and alternative finance (15 companies), and personal finance management and literacy, accounting and expense management, and payroll and benefits, each with nine companies.

Egyptian fintech startups by sub-sectors, Source: Egypt Fintech: Landscape Report 2021, Fintech Egypt

Looking at Egyptian fintech startups’ business models, the report notes the prevalence of business-to-business (B2B) and business-to-business-to-consumer (B2B2C) models, with 48 and 31 companies, respectively. This prevalence can be partially explained by Egypt’s large pool of micro, small and medium-sized enterprises (MSMEs), which make up for over 90% of all enterprises in the country.

These businesses are eager to embrace innovative fintech solutions that address their payments, cash management, financing and supply chain needs, at a time when COVID-19 is accelerating the shift to digital channels and tech-enabled products and services, the report says.

Fintech growth drivers

Out of Egypt’s current population of about 102 million, an estimated 9 million people use products and services provided by local fintech companies, the report says, translating to a rather promising penetration rate of 8.8%.

Several drivers were identified as fueling the growth of fintech in the country. For one, Egypt is home to a large market with an unbanked population of almost 50% and a mobile Internet userbase of 57%.

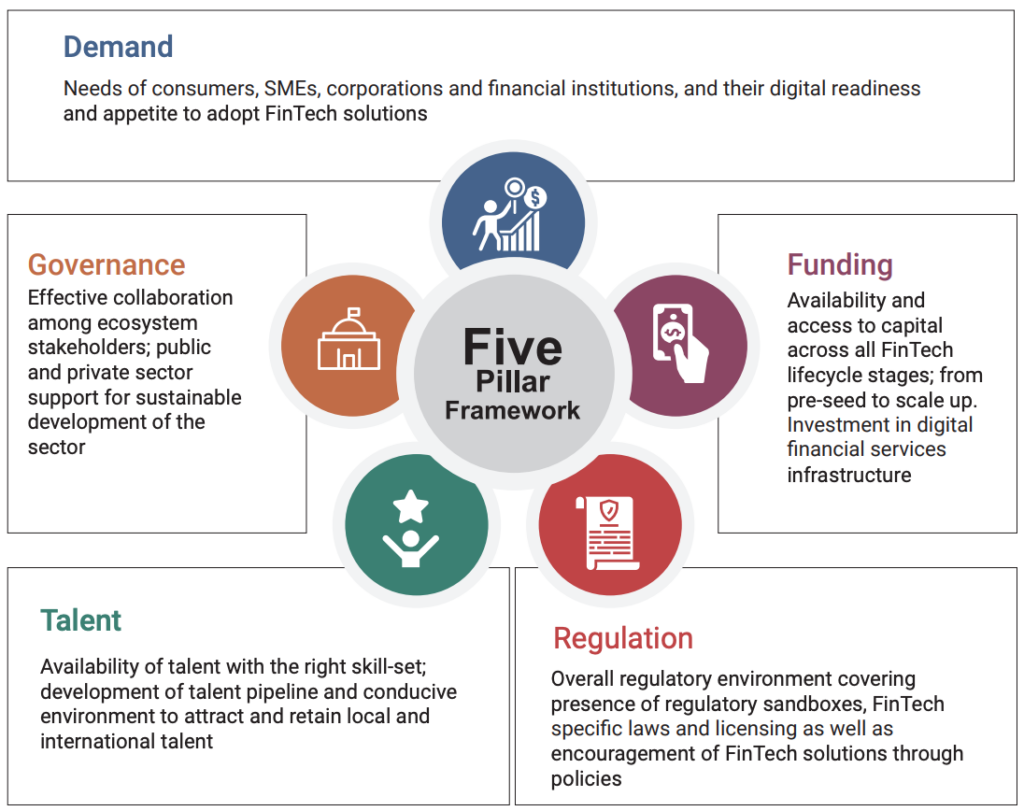

Second, the government has committed to helping develop the banking tech and fintech sectors as part of a broader digital economy push. This has translated to initiatives such as the establishment of the National Payment Council (NPC), which is responsible for overseeing and coordinating nation-wide efforts to achieve the goals of digital transformation and improve financial inclusion, the introduction of the so-called “less cash” framework, which focuses on encouraging citizens to pay digitally, and the launch of the Fintech and Innovation strategy by the central bank back in 2019, which seeks to position Egypt as “a globally recognized fintech hub in the Arab world and Africa.”

32 strategic initiatives were identified across the five-pillar Fintech and Innovation framework, and include effective collaboration among ecosystem stakeholders, availability of talent, access to capital across all fintech startups’ lifecycle stages, and conducive regulation through, for example, sandbox regimes, specific laws and licensing frameworks.

32 strategic initiatives across the five-pillar Fintech and Innovation strategy, Source: Egypt Fintech: Landscape Report 2021, Fintech Egypt

Several new initiatives have introduced over the past year, setting the stage for further growth in the coming years. These include the EGP 1 billion (US$63.6 million) Fintech Fund, the Digital Financial Literacy Strategy, as well as amendments to the Mobile Payments regulations to support digital lending using behavioral scoring and digital savings schemes on mobile money wallets.

{kind=link}

No Comments so far

Jump into a conversationNo Comments Yet!

You can be the one to start a conversation.