Embedded finance is a booming trend that’s rising all over the world, a phenomenon that’s only expected to increase moving forward as consumer demand for financial services to be delivered at their point of need in an easy and quick manner continues to rise, a new survey conducted in July 2022 and commissioned by digital finance solution provider Additiv shows.

The study, which polled 3,512 consumers from the United Arab Emirates (UAE), the UK, Germany, Sweden, Indonesia and the Philippines, found that consumers have little loyalty to traditional financial services providers and are willing to switch to non-financial service providers if more innovative services are provided.

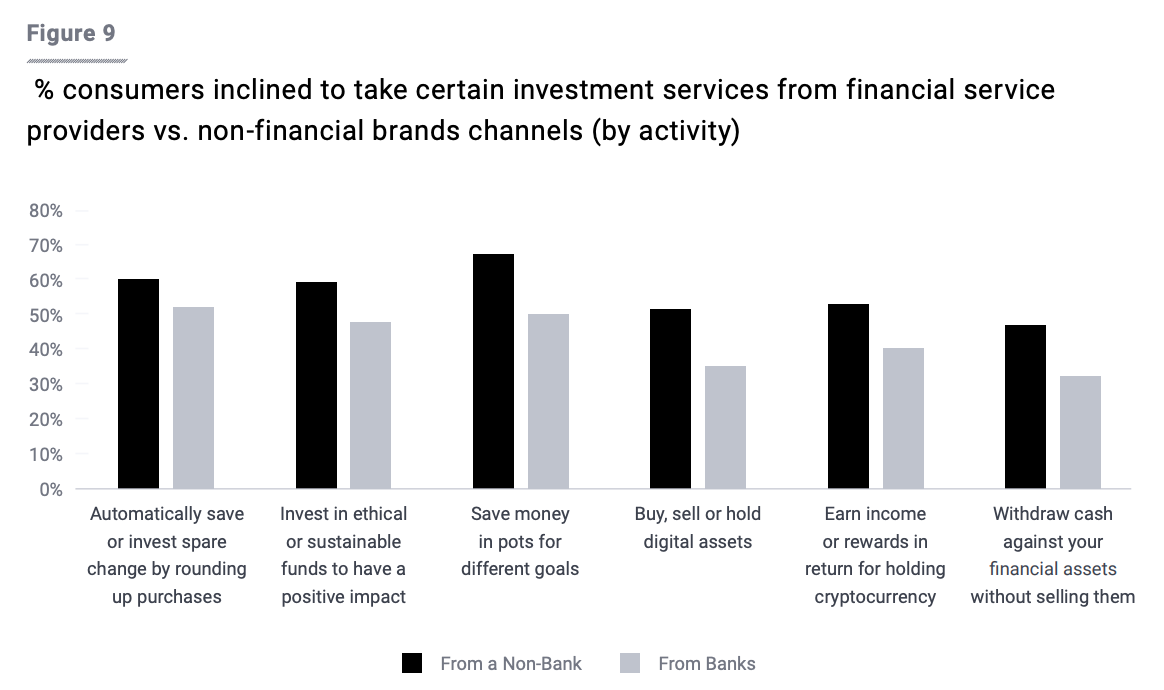

Of the consumers polled globally, 56% said they would change from a bank to a non-financial brand channel if the latter provided more convenient services. The same proportion said they would be open to take investment services through non-financial services channel.

Percentage of consumers inclined to take certain investment services from finance vs non finance brands, Source: Additiv, 2022

In the UAE in particular, the study found high interest in innovative embedded payment methods and embedded insurance products.

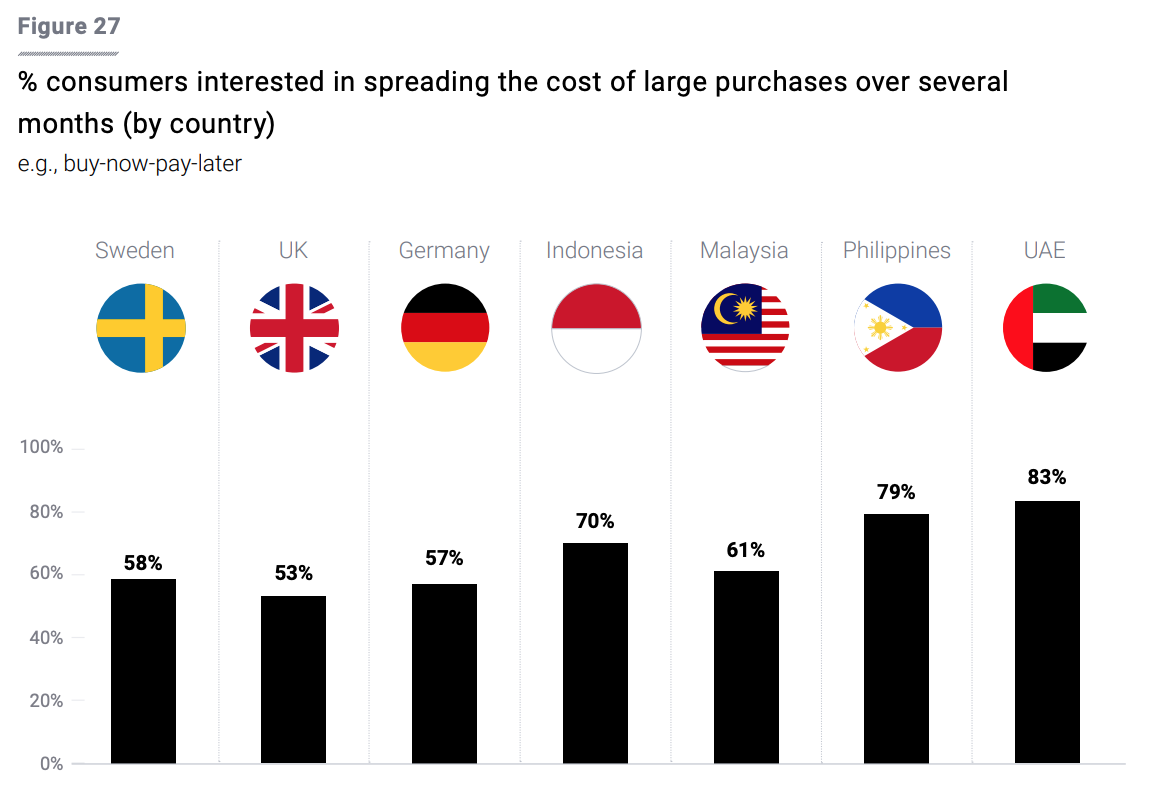

Compared to other markets, UAE consumers were found to be much more interested in buy now, pay later (BNPL) arrangements than their counterparts, with 83% sharing interest in spreading the cost of large purchases over several months, 17 points more than the global average of 66%.

BNPL, a type of short-term financing that allows consumers to take purchases and pay for them in installments, often interest-free, has surged in popularity in the UAE due to COVID-19 and the exponential growth of e-commerce.

According to business consultancy RedSeer, 10% of UAE online consumers used BNPL arrangements in 2020. This percentage is projected to rise to 30% by 2026, accumulating more than US$2 billion in consumer credit.

Percentage of consumers interested in spreading the cost of large purchases over several months (by country), Source: Additiv, 2022

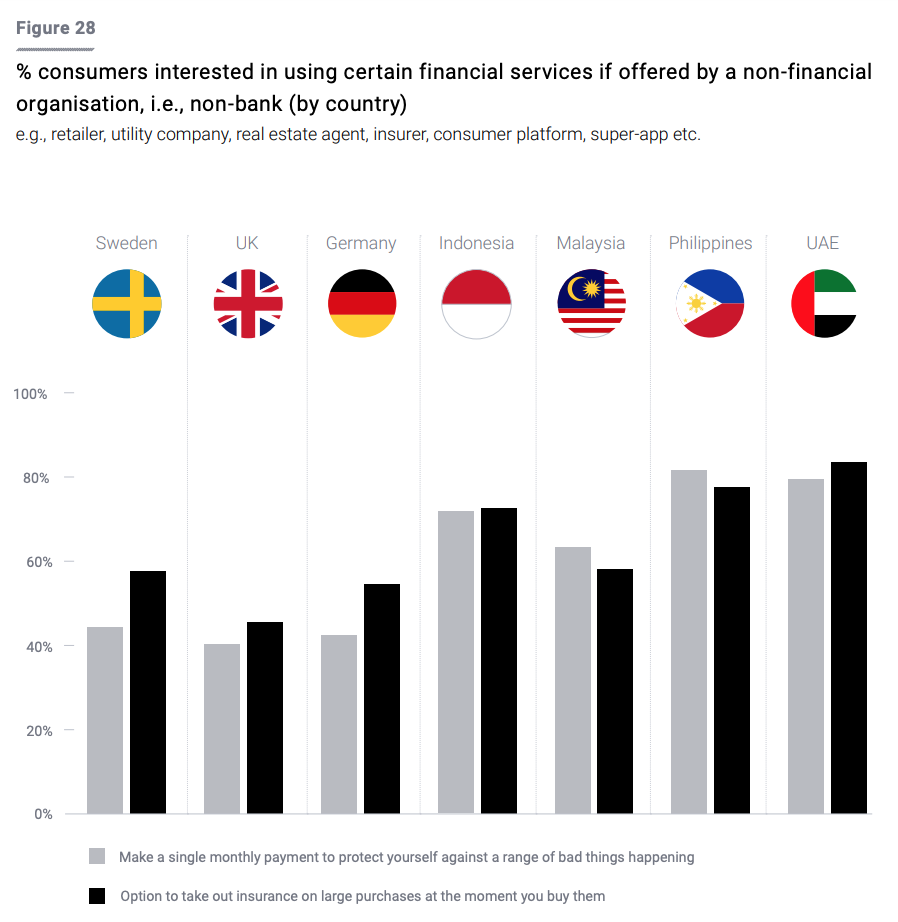

UAE consumers also showed a bigger appetite for embedded insurance, with about 80% of respondents indicating being interested in the ability to purchase insurance while buying another product or service, a 16 point increase from the global average of 64%.

Percentage of consumers interested in using certain financial services if offered by a non-financial organisation, i.e., non-bank (by country), Source: Additiv, 2022

Results of the Additiv study echo those found by other similar surveys which revealed high interest from UAE consumers to purchase relevant and personalized insurance when and where they need it most.

A 2021 consumer survey by embedded insurance provider Cover Genius and Momentive.ai, found that of those who had purchased travel insurance through a travel provider or agent in the last 12 months, 68% said they would use them again for their next trip, a figure that reveals a high level of satisfaction among those who have purchased insurance when booking their trips.

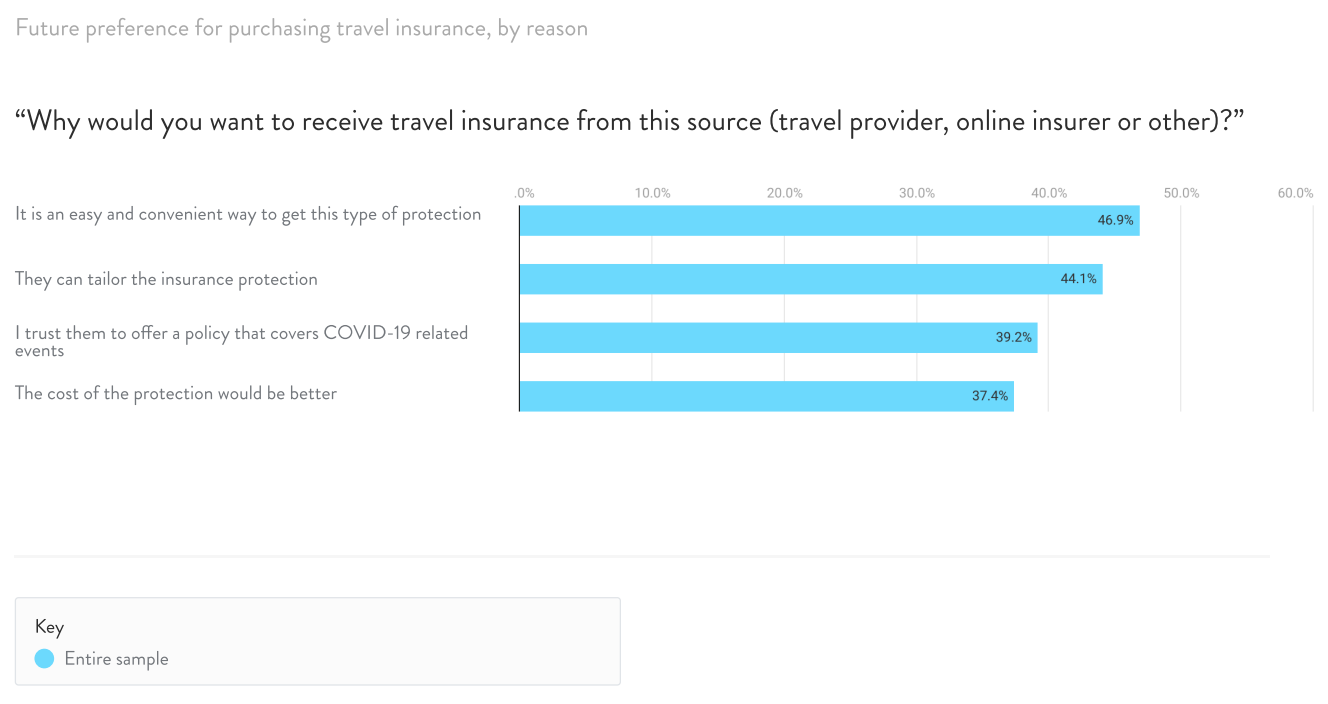

UAE consumers were also asked about their preferences for future travel insurance purchases, to which respondents indicated ease and convenience in getting protection (49%) as their top priority, followed by tailored protection (44.1%), policies that cover COVID-19 related events (39.2%) and the price of coverage (37.4%).

Future preference for purchasing travel insurance, by reason, Source: Covergenius 2021

Rising interest in embedded finance in the UAE and the broader Middle East and North Africa (MENA) comes at the time when regulators across the region are ramping up efforts for open banking adoption, a new report by the MENA Fintech Association’s Open Finance Working Group notes.

The Central Bank of Bahrain launched its open banking framework in October 2020, the Saudi Central Bank issued its framework in November 2022, and in the UAE, the Dubai Financial Services Authority has granted the first open banking related license within the Dubai International Financial Centre freezone. These three jurisdictions have been recognized as the region’s frontrunners in open banking implementation.

By establishing data sharing standards, and, in some cases, mandating banks to provide third parties with the capabilities to access their customers’ data, open banking regulations are setting the foundations for fintech innovation and new products and services to be introduced to the market.

Trends like embedded finance and banking-as-a-service (BaaS), where banking products are provided to non-bank third parties through APIs, are direct results of the open banking movement, and are now providing businesses of all types with the opportunity to offer banking services to their clientele, access additional revenue streams, and above all, offer superior user experiences through contextual and relevant products that are seamlessly integrated into the checkout process.

In emerging markets, industry participants have also pointed out to the potential of embedded finance to improve financial inclusion, noting, for example, the case of BNPL arrangements and their potential to serve those who are not eligible for traditional credit.

For the unbanked, embedded finance can provide them with the means to digitally store money, make cross-border payments, and possibly even invest, with nothing more than a smartphone and an Internet connection.

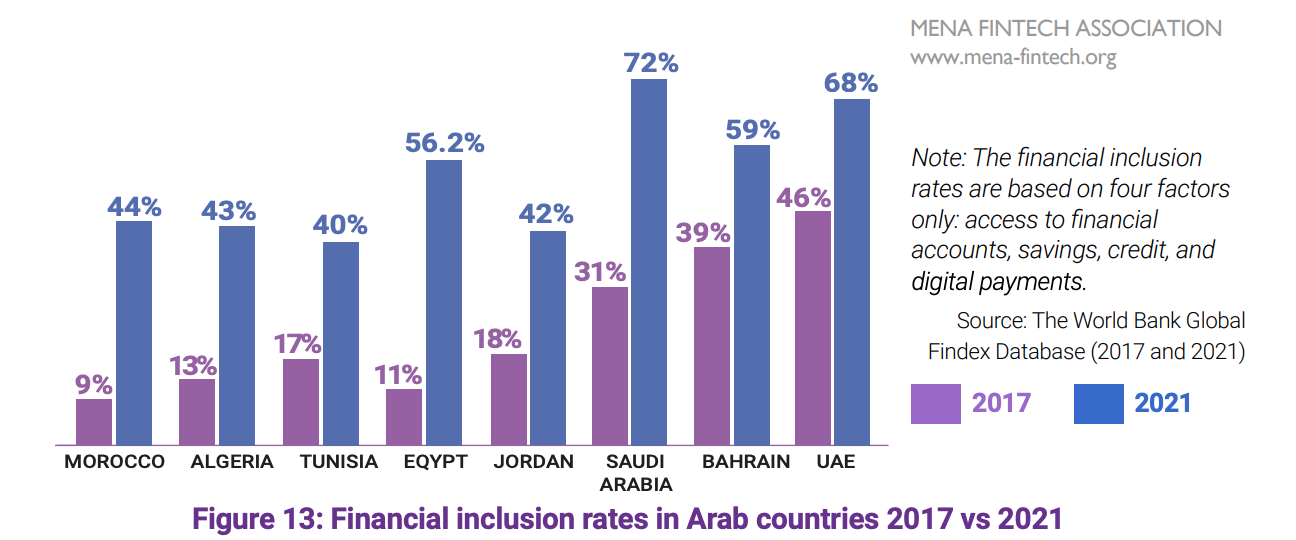

In MENA, financial inclusion rates differ greatly from one market to the other. Saudi Arabia and the UAE have the highest penetration rates of banking services and digital payments, standing at 72% and 68%, respectively, according to the MENA Fintech Association report.

At the other end of the spectrum are Tunisia, Jordan and Algeria, with just 40%, 42% and 43% of the adult population, respectively, indicating having access to financial accounts, savings, credit and digital payments in 2021.

Financial inclusion rates in Arab countries 2017 vs 2021, Source: Embedded FInance in the MENA Region, MENA Fintech Association, 2022

{kind=link}

No Comments so far

Jump into a conversationNo Comments Yet!

You can be the one to start a conversation.