In the wake of the COVID-19 pandemic, the financial sector, including Islamic banks in the United Arab Emirates (UAE), has swiftly adopted digital innovations including artificial intelligence (AI), e-learning and blockchain. These technologies are now playing a critical role in enhancing customer service and achieving sustainability goals, a new report by the Central Bank of the UAE (CBUAE) says.

The report, titled UAE Islamic Finance Report 2023 and released on December 20, 2023, looks the performance of various Islamic finance sectors, initiatives and activities globally and locally over the past year, with a specific focus on sustainability. The report provides an overview of the legislative, regulatory and Shariah governance landscape, gives an assessment of the sustainability strategies adopted by Islamic financial institutions, and looks at the different initiatives put in place to encourage digital innovation.

According to report, Islamic banks in the UAE are embracing digital innovation at a fast pace, implementing customer-related digital initiatives and utilizing cutting-edge technologies to address the changing banking landscape and evolving customer expectations.

These initiatives involve the introduction of online finance and contactless payments, the establishment of online chat support, active presence on social media platforms, the launch of dedicated applications, and the upgrade of automatic teller machines (ATMs) and cash deposit machines (CDMs). These efforts have led to a surge in online and mobile transactions, an uptick in the number of digitally-engaged customers, a general expansion of the customer base, and a higher rate of mobile wallet adoption, the banks reported.

UAE Islamic banks are also incorporating technologies like AI and robotics for facial recognition in account openings and know-your-customer (KYC) identity verification. Additionally, they are leveraging e-learning platforms for employee training and certification. Finally, blockchain technology is being used in trade finance to enhance transparency, privacy and trust between organizations.

Findings from the CBUAE study align with other research indicating that Islamic banks across the globe are developing digital transformation strategies. A 2022 report by Hong Kong strategy consulting firm Quinlan and Associates looks at the growth of Islamic banking worldwide and explores how these financial institutions are adapting to digitalization.

Recognizing the demand for digital banking solutions, several Islamic banks have launched their own spin-off version of virtual banks. Examples include Mashreq’s Mashreq Neo from the UAE, Gulf International Bank’s Meem in Saudi Arabia and Bahrain, and Bank BTPN’s Jenius in Indonesia.

In addition, several leading Islamic banks have initiated their digital transformation journeys in order to enhance revenue, improve customer experience, and optimize cost, emulating the actions of global incumbents. In Malaysia, Bank Islam became in 2021 the first bank in the country to deploy a mobile onboarding channel for retail customers that provides the first end-to-end account opening experience. In Kuwait, Kuwait Finance House (KFH), the world’s second-largest Shariah-compliant bank, has been using robotic process automation (RPA) since 2019 to automate retail credit applications and underwriting.

Digital transformation efforts of notable Islamic banks, Source: Islamic Banking 2.0: Future-proofing Islamic banks for the digital age, Quinlan and Associates, January 2022

UAE Islamic finance sector sees strong growth

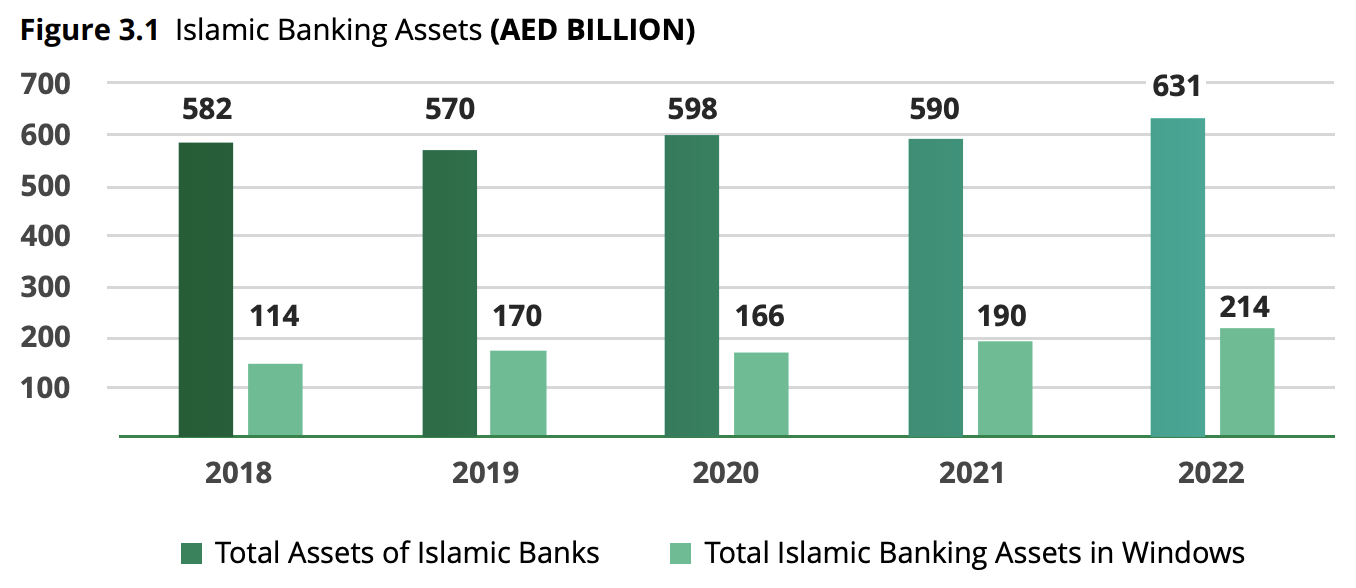

In 2022, Islamic banking continued to grow to become an integral part of the UAE’s financial industry. That year, the Islamic banking sector accounted for 23% of total banking assets within the UAE, equivalent to AED 845 billion (US$230 billion), according to the CBUAE report. The figure represents a compound annual growth rate (CAGR) of 3% between 2018 and 2022.

Like previous years, Islamic banks held the lion’s share of Islamic banking assets, totaling AED 631 billion (US$172 billion) and growing by 8% from 2018. Meanwhile, Islamic windows, which are the department of conventional banks offering Islamic or Shariah compatible financial products and services, held AED 214 billion (US$58 billion) worth of Islamic banking assets in 2022, accounting for 25% of total Islamic banking assets in the UAE and representing a stronger growth rate of 49% from 2018.

Islamic banking assets in the UAE (AED billion), Source: UAE Islamic Finance Report 2023: The Year of Sustainability, Central Bank of the UAE, Dec 2023

The UAE was home to a total of 24 Islamic banking institutions in 2022, eight of which were standalone while 16 were Islamic windows of conventional banks. Breaking these numbers down, there were six locally incorporated standalone Islamic banks and two branches of foreign Islamic banks that year, in addition to 11 local and five foreign banks with Islamic windows.

These numbers were down from nine standalone Islamic banks and 18 Islamic windows in the UAE in 2018 due to the acquisition of Noor Bank by Dubai Islamic Bank in 2020 and other mergers.

Islamic bank in the UAE snapshot (2022), Source: UAE Islamic Finance Report 2023: The Year of Sustainability, Central Bank of the UAE, Dec 2023

According to the report, the UAE’s Islamic finance industry is playing an increasingly active role in the global sustainability movement. This is in part due to the substantially alignment of Shariah principles with the objectives of the United Nations’ Sustainable Development Goals (SDGs).

An illustrative measure of this progress is the rapid growth of sukuk issuance following environmental, social and governance (ESG) principles.

Sukuk are Shariah-compliant bond-like instruments used in Islamic finance. Sukuk were developed as an alternative to conventional bonds which are not considered permissible as they pay interest, and may also finance businesses involved in activities not permitted under Shariah such as gambling, alcohol and pork.

At the end of Q3 2023, outstanding ESG sukuk in the UAE reached US$6.4 billion, up by 41% quarter-over-quarter (QoQ), Fitch Ratings estimates. In Q3 2023, about 80.6% of ESG sukuk issuance across all countries came from the UAE, showcasing the country’s leadership position in the domain.

According to the CBUAE report, the UAE is the world’s fourth largest market in term of sukuk issuance and outstanding, supported by the presence of notable Islamic financial institutions. In H1 2023, sukuk issuance reached AED 28.7 billion (US$7.8 billion) in the UAE, up from AED 24 billion (US$6.5 billion) in 2022. Sukuk outstanding grew 15% from AED 187.0 billion (US$51 billion) in 2022 to AED 215.24 billion (US$59 billion) in the first half of 2023.

Sukuk issuance in the UAE, Source: UAE Islamic Finance Report 2023: The Year of Sustainability, Central Bank of the UAE, Dec 2023

Featured image credit: Edited from Unsplash

{kind=link}

No Comments so far

Jump into a conversationNo Comments Yet!

You can be the one to start a conversation.