In Africa, South Africa, Nigeria and Kenya have the three most developed fintech ecosystems, combining more than 450 companies. This burgeoning industry has been driven by strong demographic indicators, increased connectivity, early regulation, and proactive governments.

South Africa: an early mover in fintech regulation

South Africa was an early mover in fintech regulation and development, welcoming digital innovation and supporting electronic money solutions as early as 2009, says the Africa Fintech State of the Industry 2020 report, produced by Africa Fintech Summit in partnership with EFG EV Fintech.

Ethiopia Market Map, Africa Fintech: State of the Industry 2020, Oct 2020

This supportive stance accelerated in recent years and have translated to initiatives such as the introduction of a fintech program, a fintech regulatory sandbox, as well as the launch of Project Khokha in 2017, a proof of concept project by the South African Reserve Bank that simulated a “real-world” trial of a distributed ledger technology (DLT)-based wholesale payment system using a tokenized South African rand.

Data differ from one source to another, but it is estimated that South Africa is home to about 200 fintech companies that cover a wide range of products from insurtech and cryptocurrency, to lending and wealthtech.

Payment and remittances are currently the fastest growing sector, mainly due to the growth of e-commerce and the rapid expansion of the Internet, according to a recent research paper by the Flanders Investment and Trade. Third-party payment products and payment services providers (PSPs) make up for most of the segment, with players such as Yoco, which provides a card reader and app that allows users to turn smartphones into payment terminals, and Zoona, a mobile technology company specializing in money transfers, electronic voucher payments and agent payments.

Lending is another fast-growing fintech segment with several homegrown South African fintech startups serving both small and medium-sized enterprises (SMEs) and private individuals. These include Pollen Finance, one of the largest online lending platforms in the country, as well as Lulalend, and Fundrr, two other SME lending startups.

In savings and investments, South Africa is represented by companies such as Prospa, a mobile savings portfolio for low-income populations, and 22Seven, a personal financial management app that aggregates money accounts.

The fast-maturing industry has also seen signs of consolidation with for example banking-as-a-service provider Ukheshe acquiring Oltio from Mastercard last year. Oltio developed the digital payments platform for Masterpass, Mastercard’s QR code payments service.

Nigeria: Africa’s most dynamic fintech ecosystem

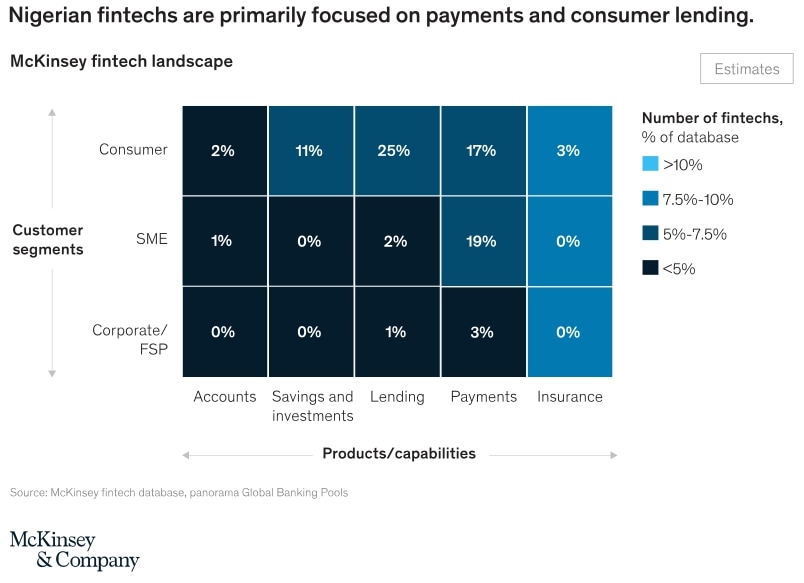

Nigeria, Africa’s largest economy with a population of 200 million, is home to Africa’s largest fintech ecosystem and an estimated 200+ fintech standalone companies, according to research by McKinsey.

These companies include some of Africa’s most valuable fintechs including unicorns paytechs Flutterwave and Interswitch.

Like South Africa, the Nigerian fintech sector has also seen a handful of exits. Last year, Paystack, an online and offline payment startup, was acquired by Stripe for over US$200 million. Paystack serves around 60,000 customers, including small businesses, larger corporates, fintechs, educational institutions and online betting companies.

Nigeria’s thriving fintech sector has been driven by the country’s youthful population, increased smartphone penetration and a focused regulatory drive to increase financial inclusion and cashless payments.

Like other markets, fintech activity initially started in payment but quickly expanded to other areas including lending, asset management, investing and insurtech.

Today, the country is home to a large pool of innovative startups that leverage cutting edge technology and digital platforms to give the public greater access to financial services and a wider range of products to choose from.

For example, in lending, startups like Carbon and Renmoney use alternative credit-scoring algorithms to provide instant, unsecured, short-term loans to individuals.

In savings and investments, companies such as CowryWise and PiggyVest offer millennials and young professionals with mobile apps that allow them to conveniently save their money and earn more interest than they would at a traditional bank. These apps also provide personal financial management tools.

Other notable fintech startups from Nigeria include Kudi, a bank agent network that aims to bridge the gap between the cash economy and digital solutions; Lidya, an online lending startup for small and medium-sized businesses (SMEs); and Kuda, Nigeria’s first mobile-only bank licensed by the central bank.

Kenya: fintech innovation stimulated by mobile money

In Kenya, fintech development has been propelled by the mobile money revolution trigged by M-Pesa, the SIM-based mobile banking service launched by telco giant Safaricom in 2007.

M-Pesa allows users to deposit, withdraw, transfer money, pay for goods and services, access credit and savings, all with a mobile device, and combines Safaricom’s mobile infrastructure with an agent model.

Since its launch, M-Pesa has spread quickly and expanded to seven countries. As of June 2020, it had more than 30 million active users in Kenya out of a total population of 52 million, according to data from the Communications Authority of Kenya.

M-Pesa and the rise of mobile money have been credited for helping economic development, contributing to the improvement of financial inclusion, which jumped from just 26% in 2006 to now 82.9% – the highest rate in sub-Saharan Africa.

The mobile money revolution was also the spark that ignited Kenya’s fintech fire with startups like Kopo Kopo emerging in the past years to provide solutions that run on top of popular mobile money platforms.

Founded in 2011, Kopo Kopo started as a digital platform to enable small merchants in Kenya to accept digital payments, primarily through M-Pesa, before expanding to other products including unsecured cash advances and loyalty programs.

But Kenya is also home to a number of startups that are pursuing global trends. Umba, for example, provides a full service digital banking app. Turaco is an insurtech startup that provides microinsurance products to individuals. Pezesha operates a digital platform where micro and SMEs are matched with investors, including banks, microfinance institutions and retail lenders, to secure funding.

{kind=link}

1 Comment so far

Jump into a conversation