The banking sector in the Middle East and North Africa (MENA) is anticipated to experience significant growth, a development which will be driven by rising demand for banking services, ongoing progress of digital transformation, and the expansion of digital banking, a new report by consultancy EY says.

The MENA H1 2023 Banking Report, released on October 15, analyzes banking activities in the MENA region, providing in depth insights in terms of sector insights, banking performance, outlook for the financial year and macroeconomic overview. The report highlights the path forward for the region’s banking sector, highlighting the critical role that technology and digital innovation will play in the growth of the sector.

According to the report, MENA’s financial services industry is undergoing a profound transformation driven by technological advancements, with artificial intelligence (AI), open banking and tokenization, in particular, set to accelerate the pace of change and introduce the biggest opportunities.

AI is poised to revolutionize banking by enabling financial institutions to offer faster, more efficient and personalized services to customers, the report says, with AI-driven chatbots in particular emerging as a prominent trend in the banking industry.

Other consulting firms and research organizations share these forecasts, asserting that the financial services sector represent a significant opportunity for AI in the region and stands to gain advantages such as process automation, increased productivity, and improved product offerings.

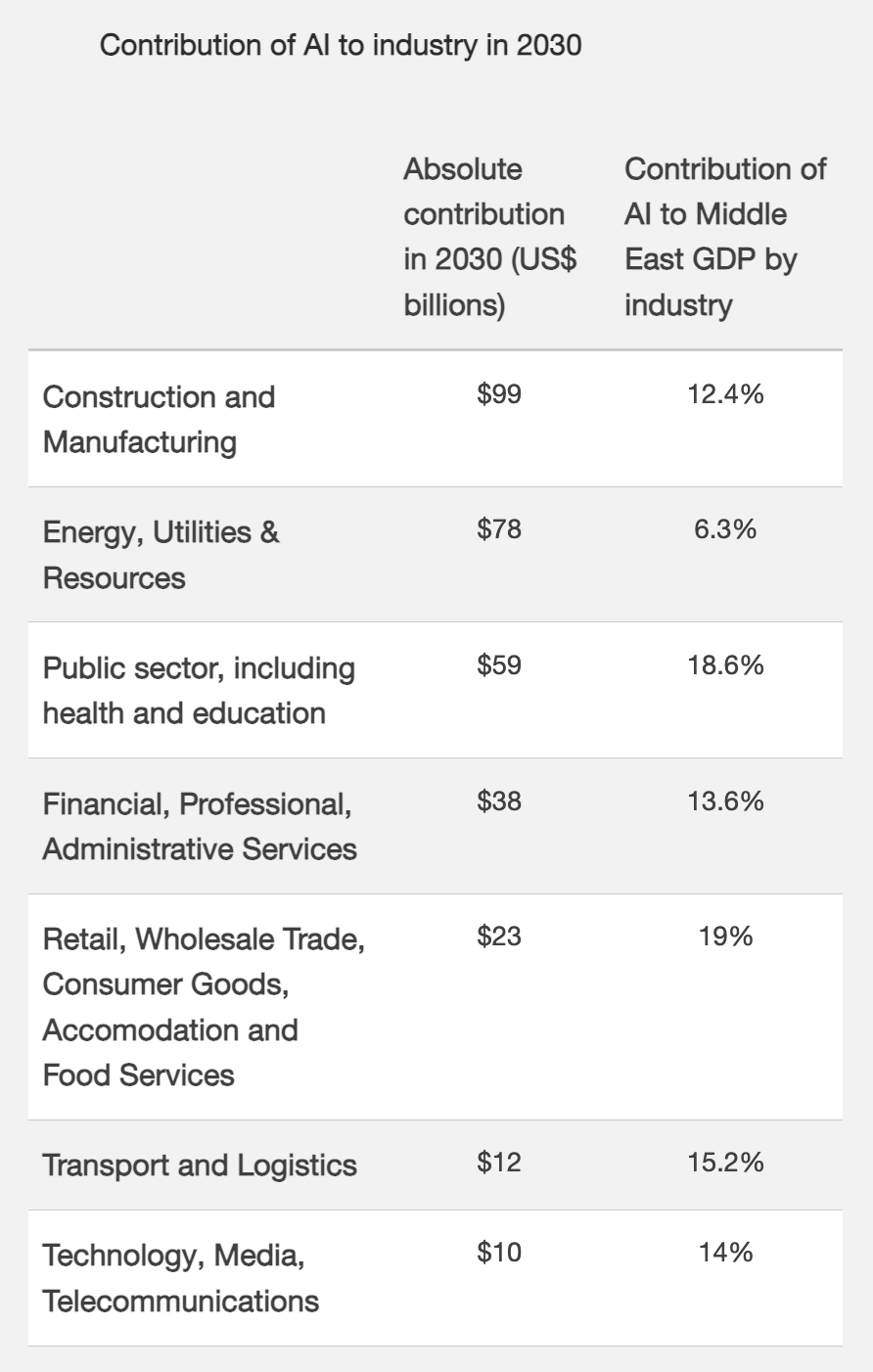

PwC predicts that AI will contribute US$38 billion to the financial, professional and administrative services sector in the Middle East and Africa (MEA) by 2030, equivalent to 13.6% of the region’s GDP.

Contribution of AI to industry in 2030, Source: US$320 billion by 2030? The potential impact of AI in the Middle East, PwC, 2018

After AI, open banking is another transformative trend that’s picking up steam in the Middle East.

Open banking, which involves the sharing of financial information, data and services through secured application programming interfaces (APIs), is creating numerous opportunities for both consumers and businesses by fostering innovation, competition and collaboration within the financial sector, the report says. It encourages continuous innovation and collaboration, ultimately helping create a more dynamic and consumer-central financial landscape.

That market has gained traction in MENA over the past years and was valued at around US$350-420 million in 2022, the Arab Monetary Fund, a regional development institution, estimates. Through 2027, the sector is projected to grow at an average compound annual growth rate (CAGR) of 25% to reach US$1.17 billion.

Tokenization is another emerging trend outlined in the EY report that’s praised for its ability to improve efficiencies, increase financial access and introduce new growth opportunities.

Tokenization refers to the process of creating a token on a distributed ledger that represents an asset. These tokens can be representations of traditional tangible assets such as real estate or agricultural, financial assets like equities or bonds, or non-tangible assets such as digital art or other intellectual property. Tokenization offers various potential benefits in the financial sector including enhanced liquidity, improved accessibility and cost reduction, and opens the door to the creation of new and innovative financial products.

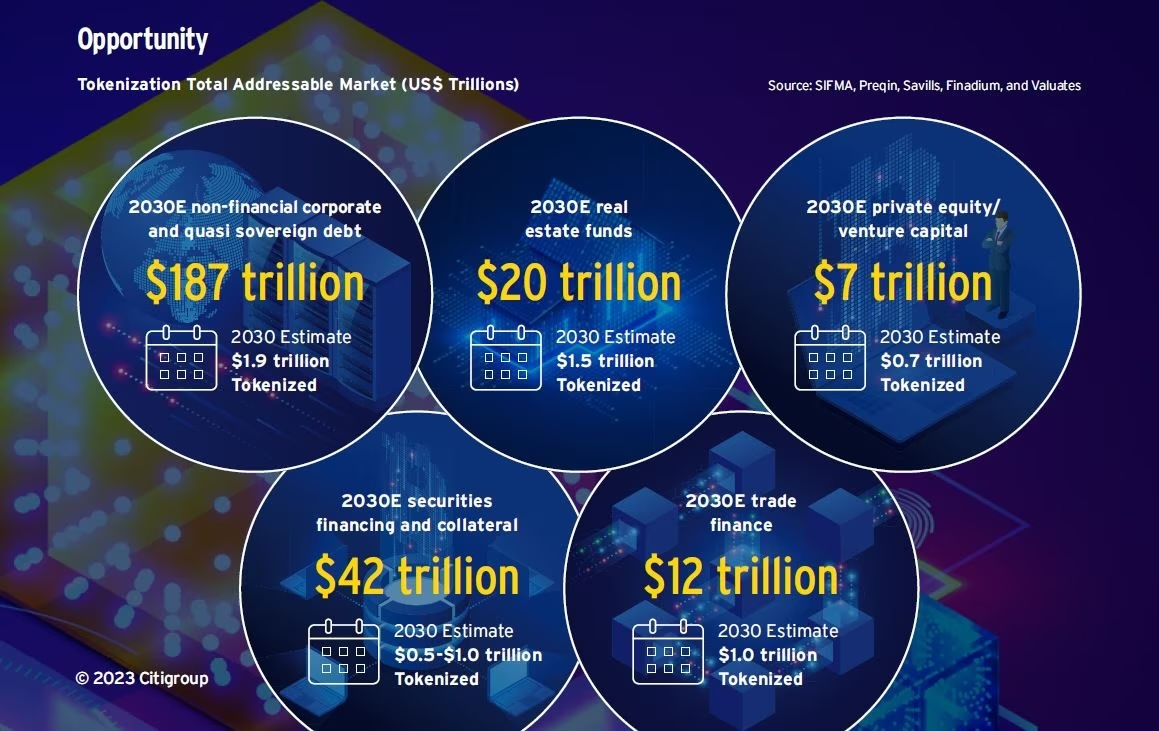

Banking institution Citi believes that tokenization could be the killer finance use case driving blockchain breakthrough, forecasting that US$4-5 trillion of tokenized digital securities could be issued by 2030.

Tokenization total addressable market, Source: Money, Tokens, and Games: Blockchain’s Next Billion Users and Trillions in Value, Citi, March 2023

Increased regulatory oversight

As global developments and technology’s increasing impact unfold, EY predicts that MENA banking and finance regulators will increase oversight and enhance reporting mechanisms over the next few years, focusing primarily on Basel IV regulations, anti-money laundering (AML), financial crime, electronic know-your-customer (eKYC), cybersecurity, open banking and digital currencies.

These initiatives will build on previous efforts from regulators to provide regulatory clarity to digital challengers, but also mitigate the risks associated with adopting new technologies and innovative business models.

In 2018, the Abu Dhabi Global Market (ADGM), an international financial center and free zone located in the United Arab Emirates’ capital, introduced the world’s first comprehensive virtual asset regulatory framework, addressing risks including market abuse, financial crime, consumer protection, technology governance, custody and exchange operations.

In Saudi Arabia, the central bank released in November 2022 a set of legislation, regulatory guidelines and technical standards to enable banks and fintech companies to provide open banking services in the country.

Egypt is another countries in the region that is making advancements in open banking. The government is reportedly discussing open banking implementation and recent regulatory initiatives such as the launch of the National Instant Payment Network (NIP), the InstaPay mobile app and the Regulatory Sandbox, are expected to boost the digital banking sector and pave the way for full open banking adoption.

Oman, meanwhile, released in September the draft of a comprehensive fintech strategy designed to support the growth of the sector through conducive regulations, industry collaborations and the development of a “national cadre of skilled and innovation-driven individuals”. The move builds on ongoing efforts on fields such as eKYC, cloud computing rules, and the development of a so-called Open Banking API Strategy.

MENA has witnessed a robust growth of its fintech industry in recent years, with funding increasing by approximately 36% annually from 2017 and 2022, according to McKinsey. By 2025, the consultancy estimates that fintech revenue in MENA and Pakistan could increase almost threefold from US$1.5 billion in 2022 to an amount between US$3.5 billion and US$4.5 billion. That growth will be driven by rising Internet and smartphone penetration, government support and regulatory initiatives, as well as growing usage from the region’s large population of unbanked and underbanked.

featured image credit: Edited from freepik

{kind=link}

No Comments so far

Jump into a conversationNo Comments Yet!

You can be the one to start a conversation.