New Report Highlights Continued Opportunities for Fintech Growth in the Middle East and Africa

22. January 2024Fintech has penetrated and transformed the Middle East and Africa (MEA)’s financial services landscape, financially including millions of people and enabling growth in other sectors.

But despite the growth, new opportunities still exist in each market to create a financial ecosystem that’s convenient, synergistic and secure, a new report by Global Ventures, a venture capital (VC) firm based in the United Arab Emirates (UAE), says.

The report, which builds on the learnings from the firm’s first previous report in 2020, provides an overview of the fintech landscape in the MEA region, highlighting key takeaways, trends and developments since the last iteration of the report. As the industry matures, the 2023 paper focuses on the next wave of development, Fintech 2.0, offering an overview of the opportunities that will characterize the sector’s next phase of growth, and emphasizing an impending momentum across payments, lending, next-generation banking and banking infrastructure.

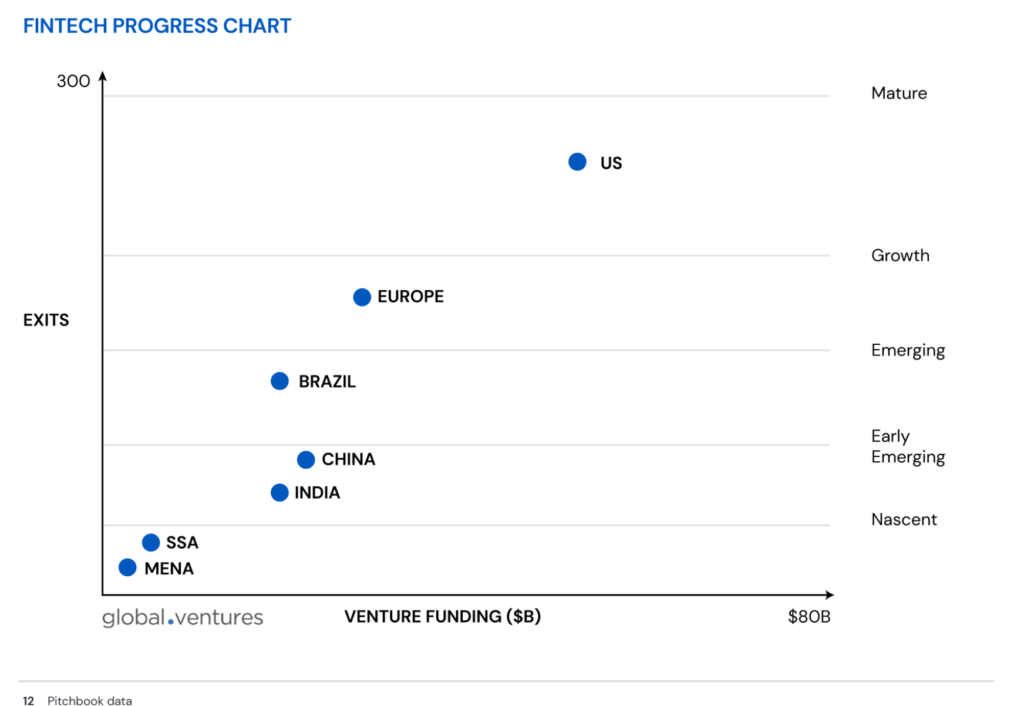

Over the last five years, MEA has witnessed rapid growth in fintech, with almost US$6 billion invested in 1,181 fintech startups across the region. The rapid growth of fintech in MEA is evident in the increasing number of mega-deals and unicorns emerging in the region, such as Fawry’s US$1.8 billion initial public offering (IPO), Tabby’s US$200 million Series D and Flutterwave’s US$170 million Series C.

This growth is also evidenced through the rise of mobile money usage and advancements in financial access. In Sub-Saharan Africa (SSA), in particular, fintech has expanded access to financial services for underbanked and unbanked populations, with account ownership more than doubling between 2011 and 2021 from 23% to 55%. According to the report, studies have also shown that, in the context of SSA, with 1% of people having access to fintech tools, there is an improvement in the financial inclusion rate of about 0.7%.

But despite recent progress, underserved and emerging opportunities still exist in each market, with the fintech sector’s share of financial services revenue standing at a mere 1% in Middle East, North Africa, and Pakistan (MENAP), and fintech penetration reaching only 3 to 5% in Africa, the report notes.

Fintech outlook in MEA

Over the next five years, Global Ventures expects a wave of regional tailwinds to transform the financial services industry in MEA. These tailwinds, driven by factors such as historical progress in financial infrastructure, favorable demographic factors, and conducive regulatory frameworks, are poised to create fresh opportunities in the fintech sector.

In SSA, more mature markets such as Nigeria and South Africa will witness innovation in more advanced financial services including business-to-business (B2B) liquidity and regtech technology such as anti-money laundering (AML) and know-your-customer (KYC) compliance. In countries where financial systems and infrastructure are still growing, the next stage of fintech will focus on financial services such as underwriting, servicing, embedded finance and buy now, pay later (BNPL) services in retail and SME segments, the report says.

Looking more specifically at key fintech segments, the report emphasizes that fintech in SSA will see growing momentum across payments, lending, next-gen banking and banking infrastructure.

In the next five years, mobile and digital wallets that built on the progress in financial inclusion witnessed in the first wave, will further transition rural and underserved communities to digital rails through payment infrastructure, the report says. Digital business-to-business (B2B) payments will further pick up steam, boosting business efficiency and expanding access to financial services for small and medium-sized enterprises (SMEs).

In lending, the report notes that consumer lending products are still largely untapped and underserved, presenting opportunities for growth. Business models such as software-as-a-service (SaaS) will see traction, with increased demand from lenders over the potential of accelerating time to market. Additionally, as digital payments continue to expand, new product offerings including salary on demand and BNPL will witness increased usage and development.

In next-gen banking, Global Ventures expects digital banks with diversified offerings to shift their focus from wallets and payment services to SME financing and credit products. It also anticipates growth in digital wallet and virtual card usage as more merchants adopt mobile point-as-sale (POS) solutions.

In banking infrastructure, the report emphasizes the rise of the aggregator model for banking-as-a-service (BaaS) offerings as market players seek to replicate the formula behind Flutterwave’s success. It also highlights the impending emergence of API-based products as new open banking frameworks get rolled out across the region.

In MENAP, the breadth and diversity of the fintech landscape means that offerings will deepen their presence and impact across the industry moving forward. In the next five years, Global Ventures predicts growth in B2B and cross-border digital payments solutions for SMEs, allowing for improved customer journeys and digital KYC solutions, and enabling improved data security.

In lending, countries part of the Gulf Cooperation Council (GCC) will see growing usage of BNPL SaaS as installment loans gain further traction and get embedded into more offerings. In addition, a growing base of institutional lenders will increase while-label SME lending offerings. In Egypt and Pakistan, financial players will embrace eKYC solutions for full digital onboarding experiences and credit assessment.

In next-gen banking, GCC nations will see neobanking players tap into open banking capabilities to expand beyond use cases of traditional banking for consumers and businesses, building features such as investments, insurance and logistics management.

Finally, in banking infrastructure, the advent of open banking in the GCC will fuel the development of new consumer-facing solutions across spend management and savings solutions. In Egypt and Pakistan, meanwhile, increased bank-fintech integration through bilateral agreements will see the development of modern tech stacks.

Featured image credit: edited from freepik

{kind=link}

No Comments so far

Jump into a conversationNo Comments Yet!

You can be the one to start a conversation.