The accelerated digitalisation that swept the globe in the last two years has led to widespread adoption of digital financial services. Customers – both individuals and businesses – now want their services fulfilled instantly, and that extends to cross-border settlements as well.

As a result, payment hubs are fast becoming the default approach for banks to manage payments. Put simply, a payments hub is a flexible platform that enables banks to build their own payments services that can integrate with multiple systems and channels, essentially breaking down the silos present in legacy structures.

In addition, these hubs enable banks to meet new requirements such as open application programming interfaces (APIs) that power open banking ecosystems.

Hubs consolidate all payment streams into a single central, standardised and coordinated platform, improving control, visibility and efficiency, as well as reducing complexity.

Regional payment hub initiatives

The Middle East and North Africa (MENA) payments space was already booming pre-pandemic, with consumer digital payments transactions in the United Arab Emirates (UAE) growing at an annual rate of more than 9% between 2014 and 2019, almost double Europe’s average annual growth of 4-5%.

An August 2021 McKinsey survey found that these impressive growth rates have been boosted further by the pandemic. Saudi Arabia’s digital point-of-sale (POS) transactions doubled in the year to January 2021, for instance.

The increased consumer demands on instantaneous cross-border payments settlement has not gone unnoticed, as regulators, organisations and central banks across the region have rolled out payment hub initiatives in recent years.

Buna is a cross-border payment system owned by the Arab Monetary Fund, a regional Arab organisation. As of January 2022, Buna had onboarded close to 30 banks and was in discussion with more than 130 banks from 13 different countries. In March 2022, Buna went one step further, taking steps to connect its payment system with China’s UnionPay International.

The Gulf Payments Company is a multilateral organisation aiming to unify the banking systems of the six Gulf Cooperation Council (GCC) members: Saudi Arabia, the UAE, Bahrain, Oman, Qatar and Kuwait. Its AFAQ platform is a joint regional payments platform linking real-time gross settlement systems for each GCC country, where the immediate processing of inter-GCC transfers is carried out at the end of the day, including total settlements.

Separately, the Central Bank of the UAE’s National Payment Systems Strategy includes the development of a National Instant Payment Platform, which will enable real-time payments and fund transfers 24 hours a day.

All these initiatives are happening concurrently with widespread migration to ISO 20022 across MENA, leading up to the November 2022 deadline. A global and open standard, ISO 20022 creates a common language for payments worldwide. And its higher quality data means better payments for all.

This means fewer errors, less manual intervention, fewer delays for the end customer and ultimately a more efficient, cost-effective and higher quality payments system and experience for all.

Finastra snags payments hub leader mantle

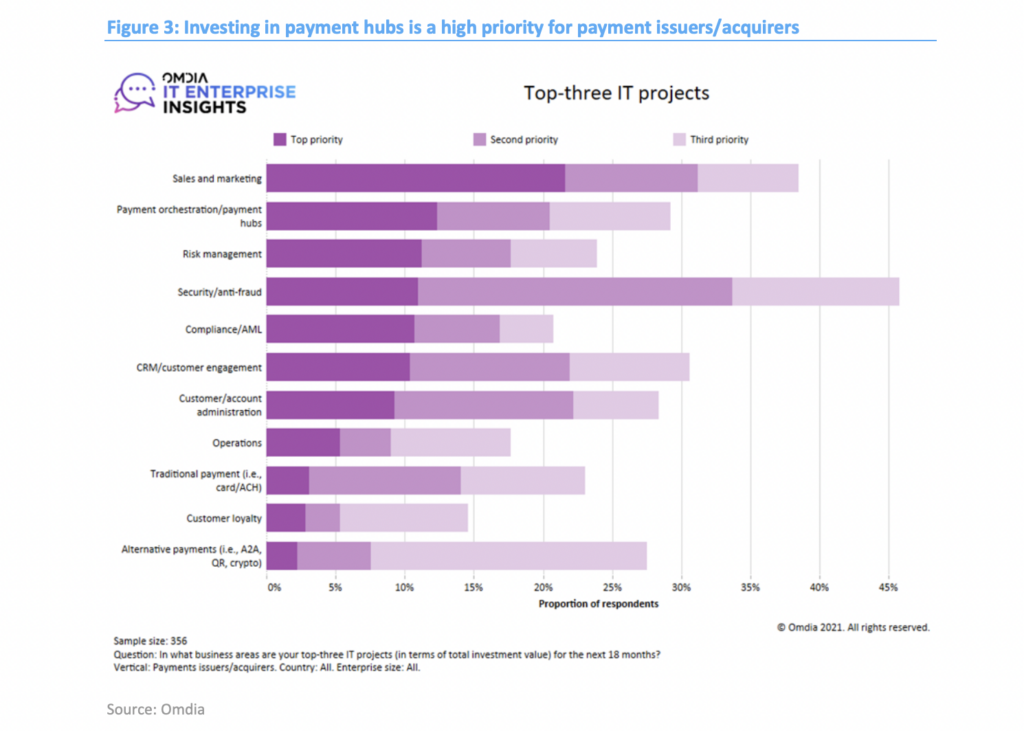

In its “Selecting a Payment Hub, 2021-22” report, technology research firm Omdia Universe estimated that by 2025, global spend on payment hubs will reach US$2.6 billion, growing at a compound annual growth rate (CAGR) of 8% between 2020 to 2025.

The 2021 study conducted by the firm, which polled payment issuers/acquirers, found that 29% of respondents identified payment hubs as one their top three IT projects.

Omdia noted that banks need to understand the capabilities and limitations of various payment hubs to implement the correct strategic approach to enable their payment transformation ambitions.

Its report also highlighted leading payment hub platforms and providers, naming London-based Finastra as a market leader due to its wide breadth of functionalities that are available off-the-shelf and can be deployed flexibly.

Supported by the broadest and deepest portfolio of financial services software, Finastra delivers this vitally important technology to financial institutions of all sizes across the globe, including 90 of the world’s top 100 banks.

Finastra has a large ecosystem of fintech partners through its collaboration platform, which is integrated with the payment hub solution. The vendor also scored highly across several categories and has been praised by customers for its excellent customer support and collaborative approach to designing its product roadmap.

Finastra’s payment hub solutions in MENA

Within the MENA region, Finastra’s payment hub offerings are led by Fusion Global PAYplus (Fusion GPP), an omnichannel payments hub, providing domestic and international order management, payment processing, and payment execution functionality across a broad range of payment instruments.

Fusion GPP primarily targets Tier 1 and Tier 2 banks, while its software-as-a-service cloud solution Fusion Payments To Go addresses payment hub needs for mid- to low-tier banks.

MENA’s payments market will only continue to grow, and so MENA banks and organisations looking to centralise and unify all their digital payments needs in a single hub, will be looking for solutions that give them scalability and flexibility to expand their offerings to respond to newer trends.

Finastra’s large partner ecosystem enables banks and fintechs to offer additional services through third parties which can be pre-configured for easy deployment, and thus can tap this partner ecosystem to broaden their platform solution capabilities.

Download Omdia’s report to help you achieve your payment transformation ambitions by selecting the best payment hub here.

Featured image credit: Edited from Unsplash

{kind=link}

No Comments so far

Jump into a conversationNo Comments Yet!

You can be the one to start a conversation.